The Fed and Recession

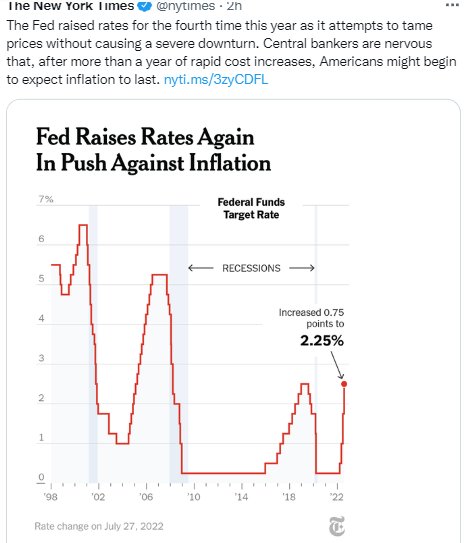

Months ago when The Fed raised rates by 75bps. Tonight, The Fed raised interest rates by 0.75%, another big jump as it continues its aggressive campaign to rein in inflation even as the economy begins to slow.

Let me admit that I had no idea what bps meant for most of my academic (as an IR scholar) and several year professional career (when to be a Legal Intern in Parliament). This was until I worked on an associate team, everyone using this term and I finally asked. 75bps isn’t quite 0.75%, it’s .75 points which are additive changes to a rate.

For example, if a sales tax goes from 2% to 3%, it’s a 50% increase in sales tax, but a 1 point, or 100 basis point, increase in sales tax. I pay attention. 75-basis point increase is an unusually large one. In the race between investment classes, U.S. bonds are starting to breathe down the stock. Median leverage for issuers of investment-grade corporate bonds already jumped 14% in the first quarter of 2022 - the biggest quarter-on-quarter jump on record, just because (afer) 75 bps by The Fed.

(after the G7 Summit in Elmau Germany. G7 and several countries like Indonesia-host G20 this year; South Africa; India; Senegal)

(after the G7 Summit in Elmau Germany. G7 and several countries like Indonesia-host G20 this year; South Africa; India; Senegal)

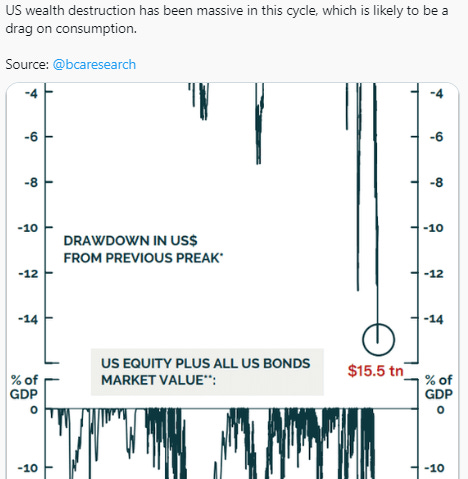

To reflect how overwhelmed the economic situation, once again, with the U.S. example. In Q1, 20% of all home purchases were bought by investors for the first time ever. This is assuming “housing” is (only) intact assets nowadays for the American. The Fed uses rates as a tool to impact demand. To get consumers to think again about spending, borrowing and investing. A brake on the economy on the demand side.

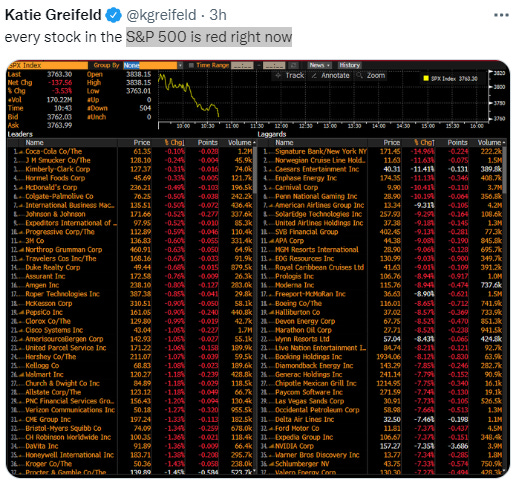

(S&P, 19 hours after The Fed announcement 75bps)

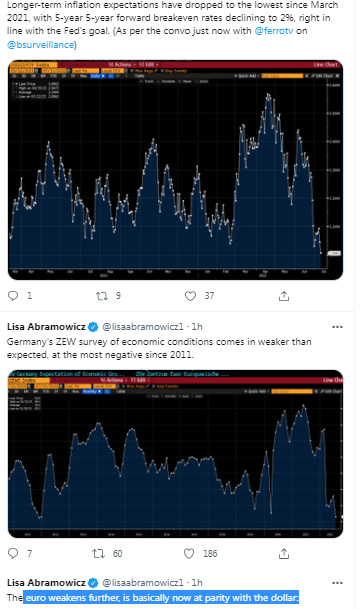

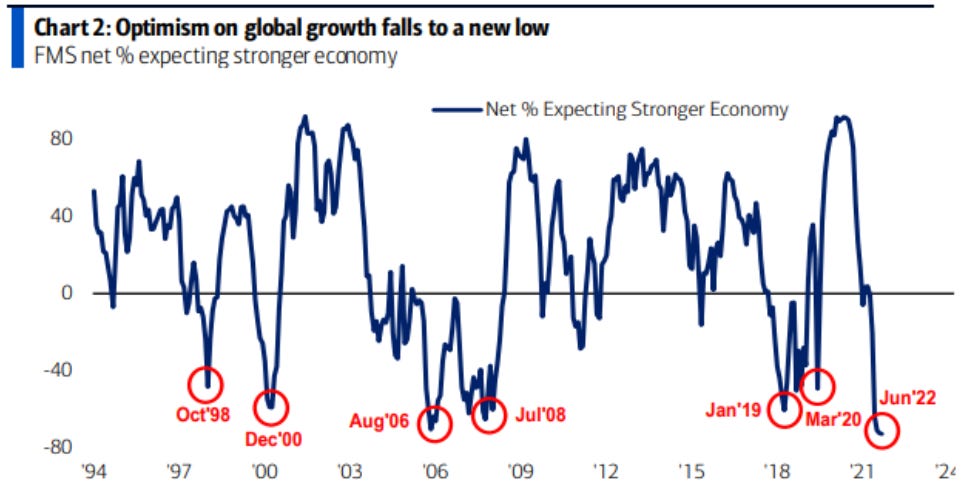

The 'quiet' selloff in corporate credit is coming back and I bet it's going to get a lot noisier than “the brutal loss” (June 13th, 2022) in Wall Street. The percentage of fund managers expecting a stronger economy falls to a new low. Dramatic moves in bond yields show that the world's most important market has a big and repetitive problem. And weakened several currencies across the world.

US investment-grade bond funds have recorded an unprecedented streak of 13 consecutive weeks of outflows, with $55.7 billion withdrawn in the period. Distressed debt and bankruptcy (especially) Crypto-Bitcoin companies will be long-term. The central bank's actions led to a (decline/rise) in equities by giving investors (uncertainty/confidence) that financial conditions would (deteriorate/stabilize) due to (rising inflation/strong GDP growth).

(June 13th)

US inflation accelerated to a fresh 40-year high in May, a sign that price pressures are becoming entrenched in the economy. That pushed The Fed to extend an aggressive series of interest-rate hikes (to be 75bps). Market always tanks when (The Fed Chairman) Jerome Powell talks.

The Fed slipped behind the curve on inflation - not entirely their fault given the external shocks of war, etc - but their job to fix it and they want the world to know it. They can’t grow food or pump oil, but they can hammer demand. The Fed Powell argues, In economic discussion generally, there's much too much focus on demand management, and not enough on things that will make us grow at the maximum sustainable level - sustainable growth - in the longer run.

We may see several reasons to suspect that inflation-focused political ads could put upward pressure on inflation expectations in the near-term. The Fed might feel compelled to respond forcefully to even moderate further increases in long-run inflation expectations. Jerome Powell voiced continued murmurs of concern on inflation expectations drifting up, some small signs, concerning signs that inflation expectations are rising.

Democrats warned against overdoing it and pressed Jerome Powell to endorse other methods. Republicans tried to get Powell to identify supply-side remedies. Powell mostly demurred. The events of the last few months around the world (unmitigated Russia - Ukraine war with no timetable/no end; re-lockdown again Beijing & Shanghai because of coronavirus; surge-rocketing coronavirus in U.S. and several countries) have made it more difficult for us to achieve what we want. But Powell reiterates over the coming months, the public will be looking for compelling evidence that inflation is moving down. The disinflationary forces of the last quarter century have been replaced at least temporarily by a whole different set of forces.

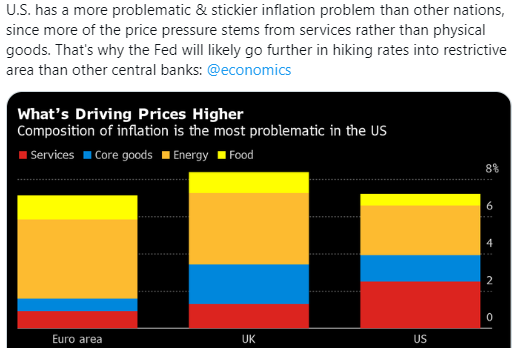

Consumer price index increased 8.6% from a year earlier in a broad-based advance (Inflation in Indonesia: 3-4%). The widely followed inflation gauge rose 1% from a month earlier, topping all estimates.

Shelter, food and gas were the largest contributors, and gas was very impactful because (effect) the Russia - Ukraine war and abruptly rocketing price of gasoline. The gap in prices between gasoline that power different parts of the global economy may never have been wider. The so-called core CPI, which strips out the more volatile food and energy components, rose 0.6% from the prior month and 6% from a year ago, also above forecasts. U.S. imports are cratering too, dropping off a cliff. U.S. small-business sentiment dips in May amid high-inflation. U.S. Retail Sales growth also falls, constrained by a plunge in auto purchases.

Seemingly terrified investors are still unwilling to sell for the “fear of missing out.“ It is worth noting that during previous bear markets, equity allocations fell as investors fled to cash. Such has not been the case in 2022. However, while estimates, and forward expectations of rising equity prices, history clearly shows that earnings do not survive recessions. Such is because earnings come from economic activity, and therefore recessions result in earnings reversions. Given that earnings expectations are at the top of the long-term growth channel, a reversion below the trendline should be no surprise.

Investors seem more afraid of missing the bottom should the Federal Reserve suddenly reverse course on monetary policy. Much like Pavlov’s dogs, after years of being trained to “buy the dip,” investors are awaiting the Fed to “ring the bell.“

However, if a recession is approaching, the question will be how deep of a price declination investors can emotionally withstand.

Prevent a cheat by oil companies amid rocketing price because the Russia -Ukraine war, Oil companies that record a profit margin better than 10% would face a new federal surtax under a plan developed by a key senator, as Democrats and the White House struggle to curb US energy costs and broader inflation. Biden has sent letters to the CEOs of the nation's largest oil companies saying he's considering invoking emergency powers to "increase refinery capacity and output" in the U.S. Biden chastised oil companies for profiteering off surging energy prices. "At a time of war, refinery profit margins well above normal being passed directly onto American families are not acceptable”, Biden’s letter to companies.

The Fed faces an immediate dilemma and a longer-term one, both illustrating how far it has let first-best policy responses slip through its fingers. Immediate dilemma has shown validate 75 bps hike and, in the process, go against its prior forward policy guidance and also contradict what Jerome Powell had ruled out. In the Longer-term, option for an aggressive policy counter to inflation and risk recession or take a softer approach and risk inflation persisting well into 2023.

The prospect of major regulatory shifts and rate in market structure is among the reasons not to pursue a stock trading platform. Current situation actually (unsurprisingly) the total amount of taker volume on the sell side surpassed the taker volume on the buy side in the stock markets. Liquidity demanders contributed to negative price movements. At least, the Central Bank of China is set to keep the medium-term rate unchanged before 75bps The Fed decision.

Somehow less investors (may) claim to have capitulated. Either way, the vast majority are hanging in there despite what it may feel unlike daily headline news about the market worldwide since the Russia - Ukraine war (Feb 24th 2022). Missing “full capitulation” piece means investors expect rate hikes not cuts; stocks prone to imminent bear rally but ultimate lows not yet reached.

Nasdaq has companies “on file,” waiting for better conditions before they tap the public markets. The yields for stocks and bonds are at an inflection point that will make it hard for investors to dive back into riskier assets. The S&P 500’s earnings yield has the smallest premium to IG bond yields since 2010 (Year 3rd after Lehman Brothers/Global Financial Crisis). Entire stock market ecology has a tough time adapting to the end of cheap (even free) money, with cash flow, rather than "valuation" being the central focus.

Policy prevented a sharper downturn but the coronavirus pandemic made the global economy hard to mitigate since 2020. Policies severely disrupted international supply chains, especially when “Global Hub” like Shanghai decided to lockdown. Inflation and negative GDP are the hangover from 2,5 years of economic insanity.

Those who entered finance after 2008 Lehman Brothers are, basically, unskilled labor. Since 2008 Lehman Brothers, Low rates caused hundreds trillion dollars of asset inflation hence unrealized gains.

With chaos in the stock market in China since March 2022 and the last 3 weeks in the U.S., we’re going to speak of a recession in existence at this point. The offset is how long it takes The Fed to reverse the recession.

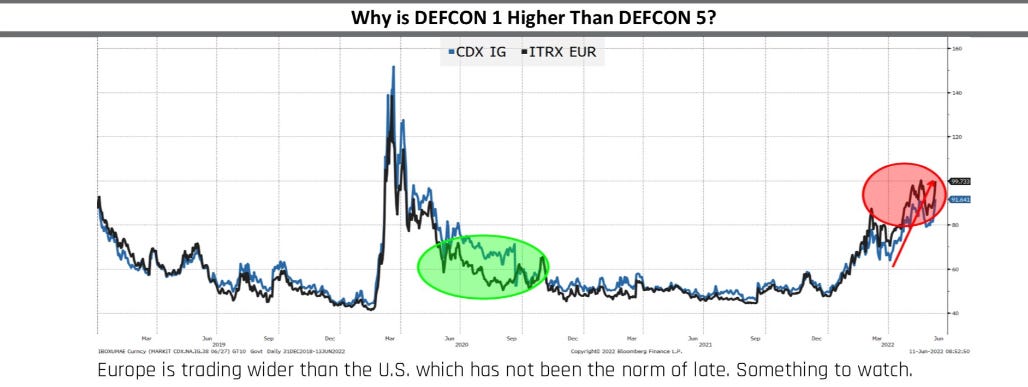

European Central Bank credit is now weakening more than US credit. As long as uncertainty and lack of clarity persist on the tools the ECB is willing to deploy against broader fragmentation arising from policy normalization, the risk is that their commitment will be tested. Has the last ECB meeting put significant doubt in Quantitative Easing support and or created fear about fragmentation being political & messy? This (high inflation, conundrum stocks market, impact because of the Russia - Ukraine war) actually to be prevented when Biden was in Europe 2 months ago when met several NATO leaders like Scholz, Macron, Draghi? ECB calls unscheduled meeting to design new bond-buying plan to tackle market turmoil, just minutes after The Fed 75bps announced. In Frankfurt, ECB has signaled what it sees as the danger zone, and as long as the fine prints are not out it may be tested again.

Financial sanctions on Russia since the war started (February 24th) won’t necessarily hurt the global importance of the US Dollar and the Euro, according to the European Central Bank. Some Biden high-rank concern that rather than dissuade the Kremlin as intended, US sanctions have instead exacerbated inflation, worsened food insecurity and punished ordinary Russians more than Putin or his allies (Saudi—-because oil; Iran—because oil & gas too; Angola—-same like Saudi & Iran).

Biden high-rank underestimated the amount of self-sanctioning companies would do, a fact that’s contributing to inflation, how to squeeze Russia given that sanctions since February (war started) don't seem to have changed Putin's strategic calculus so far.

Then, amid The Fed meeting, Corporate Bond buying is getting popular again (for now). After The Fed 75bps, Central Banks around the world are realizing hope is not a strategy. They should have realized earlier, but better late than never.

Former Chairman The Fed, Ben Bernanke, doesn’t think Bitcoin would take over “as an alternative global currency. Gold has underlying use value. The underlying use value of a Bitcoin is to do ransomware or something like that, added Bernanke.

The recent extreme moves by the Fed were both unusual and entirely predictable. The long-anticipated bear market is finally here. Hopefully after Jerome Powell (Governor The Fed) met Biden last May, 75bps Powell’s decision was a wise option about rate, amid market crumbling.

pradamulia.work@gmail.com