Missed Compliance, "They Didn't Do It": Autopsy of a bank failure, Silicon Valley Bank, the multiple warnings that were missed.

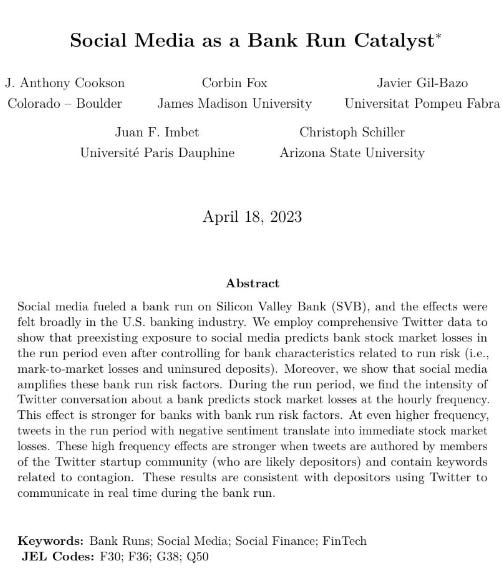

To those caught in its path, the cycle of rumour and panic that destroyed Silicon Valley Bank struck as violently as a tornado. “The speed of the world has changed,” said Sam Altman, the technology executive behind the artificial intelligence phenomenon ChatGPT, shortly after a historic bank run in which customers tried to withdraw at least one-quarter of their deposits in just over 24 hours. “People talk fast,” he added. “People move money fast.” If you are a bank, you apparently really want to avoid being interesting to social media influencers. “Banks with a large preexisting exposure to social media performed much worse during the recent SVB bank run.” Twitter conversations drove stock prices.

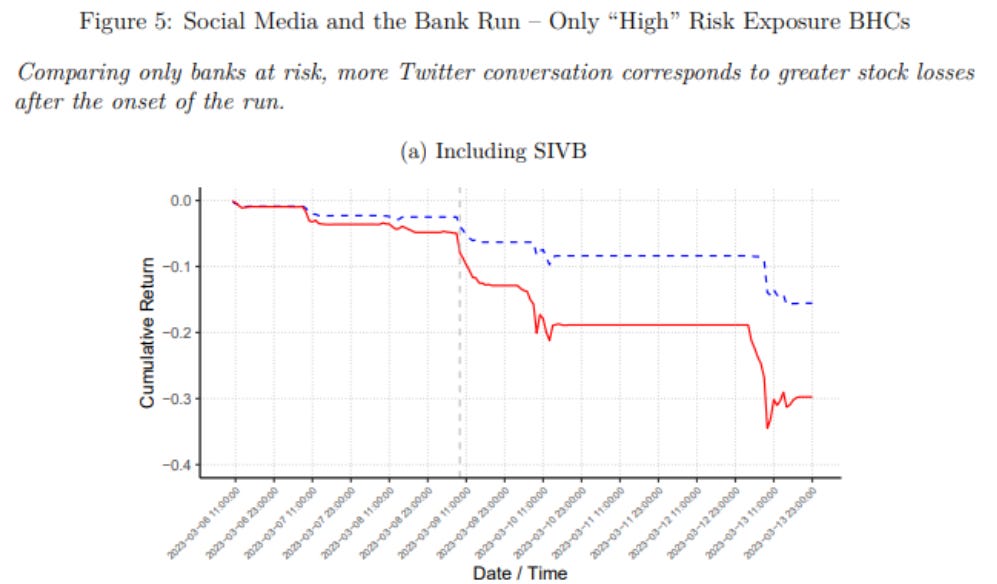

Social media amplifies these bank run risk factors. During the run period, we find the intensity of Twitter conversation about a bank predicts stock market losses at the hourly frequency. This effect is stronger for banks with bank run risk factors"

Yet the weeks since the SVB collapsed on March 10 have brought an uncomfortable realisation — the problems that provoked the biggest bank run in history were neither a freak occurrence nor an unforeseeable emergency. Mobile apps that helped people withdraw billions of dollars of deposits in just hours at Silicon Valley Bank highlight a new risk for banks’ liquidity planning, a top US regulator says

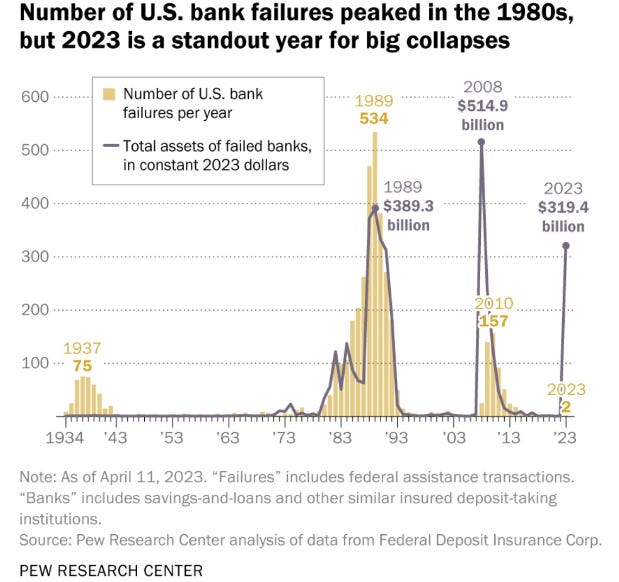

The 2023 banking crisis has had just 2 bank failures, SVB and Signature Bank, for a total of $319 billion in assets. By comparison, over 500 banks collapsed between 2007 and 2014 for an inflation adjusted $960 billion in assets. Between 1980 and 1995, more than 2,900 banks failed with $2.2 trillion in assets. If no other banks fail in this crisis, total assets involved in bank failures this year would be higher than the $389 billion in 1989, where 534 banks collapsed. History says that bank failures come in large batches which we have not seen yet in 2023. Are more bank failures coming or will we defy history? Between 1921 and 1929 an average of 635 banks failed PER YEAR. Between 1930 and 1933, 9,000 banks failed. While 2023 is nowhere near the Great Depression, having just 2 bank failures would be historic. It would mark the highest Assets/Bank Failure out of any crisis in history.

The crisis that brought down the bank had been hiding in plain sight. More than a year before the bank failed, outside watchdogs and some of the bank’s own advisers had identified the dangers lurking in the bank’s balance sheet. Yet none of them — not the rating agencies, nor the examiners from the US Federal Reserve, nor the outside consultants that SVB hired from BlackRock — was able to coax the bank’s management on to a safer path.

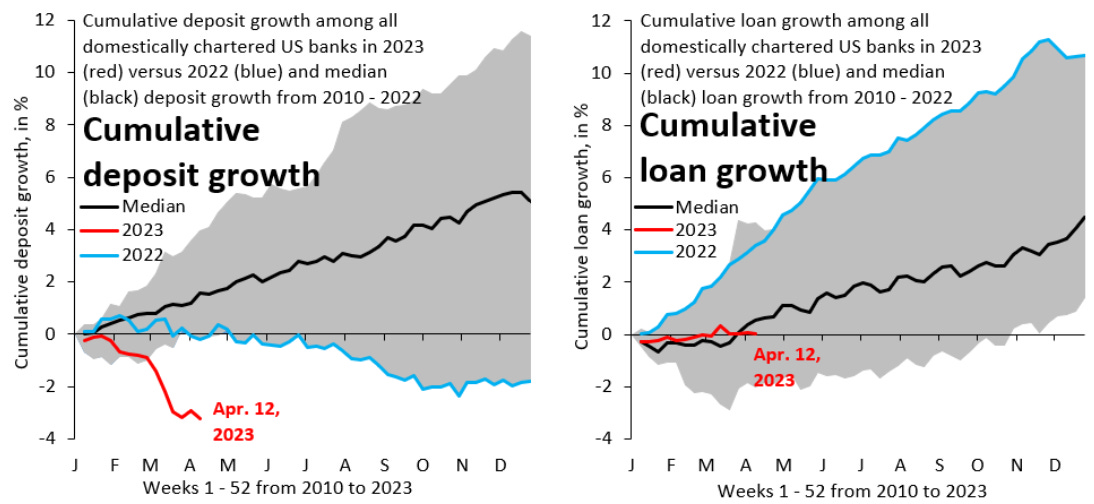

The Federal Reserve is actively considering closing a loophole that allows some midsize banks to effectively mask losses on securities they hold, a contributing factor in the collapse of Silicon Valley Bank. In the wake of SVB, US bank deposits are no longer the story, since they've basically stabilized (lhs, red). What is the story - a big story - is that loan growth has ground to a halt (rhs, red), after rapid loan growth in 2022 (rhs, blue). This "sudden stop" will weigh on GDP.

Led by vice chair for supervision Michael Barr, the Fed is considering ending an exemption that allows some banks to boost the amount of capital they report for regulatory purposes, according to people familiar with the matter. Capital is the buffer banks are required to hold to absorb potential losses.

That such obvious dangers went unheeded has dismayed the survivors of previous moments of financial peril. “I generally don’t second guess what someone should or shouldn’t have seen when I have the benefit of hindsight,” says Lloyd Blankfein, who was chief executive of Goldman Sachs during the 2008 crisis. “I’ll make an exception in this case, because the [problems] were very apparent.”

Weeks after their seizure of SVB, US regulators are still reckoning with the damage wrought. Protecting the money in SVB customers’ accounts has so far cost the authorities $20bn. To contain the disruption, vulnerable institutions have received emergency financing amounting to tens of billions of dollars more. As the Fed prepares to release what will be the first of several official postmortems next week, those responsible for keeping the US banking system safe are being forced to reckon with the magnitude of their errors. “The regulators just didn’t take a strong enough position,” says Lev Menand, a professor at Columbia University who previously worked on regulatory matters at the Treasury department and the Federal Reserve Bank of New York. “The statutory scheme empowers the Fed to override the business judgment of bank managers in these situations,” he adds. “They didn’t do it.”

The costs of those mis-steps have been compounded by the steepest rise in US interest rates in more than four decades. When regulators began talking to SVB about the concentration of long-term debt on its balance sheet nearly 18 months ago, US interest rates were close to zero.

By March, the month SVB failed, rates had reached their highest level since 2007, and the Fed’s inflation-fighting rhetoric indicated that the central bank would raise rates beyond 5 per cent this year. That sharp tightening of monetary policy all but guaranteed that SVB would suffer crippling losses on its substantial holdings of US government bonds. Signs of trouble were well within the eyeshot of depositors and regulators. Whether a crisis could be averted now depended on who acted first — the authorities and the bank’s management, or the depositors. In the public domain Rating agencies were one such source of publicly available information about the looming problems.

As early as October, S&P noted the “very large” balances of individual depositors — well above the $250,000 limit for federal deposit insurance — a factor that presented “some liquidity risk in the event of withdrawals” possibly because those depositors would be more likely to move their cash elsewhere. If that risk materialised, the agency viewed SVB as “unlikely [to] sell securities for liquidity given that rising market rates have contributed to a large unrealised loss”. That left few options, besides borrowing from the Fed or other lenders of last resort.

Even so, some critics wish the agencies had gone further. While the S&P analysis was far more critical than anything the rating agencies supplied before the 2008 crisis, it stopped short of drawing clear conclusions about SVB’s catastrophic trajectory. Neither Moody’s nor S&P had stripped SVB of its investment grade rating by the time it failed in March. “Most investors probably don’t read what [the analysts] write, they read the rating,” says one credit analyst who has extensive knowledge of rating agencies’ process for evaluating banks. “The rating needs to be where your mouth is. [Otherwise], it’s as if you would say it’s the best hotel in Paris but it has four stars instead of five.” Another important source of prescient insights came from short sellers, who by last autumn had identified potential time bombs in practically every corner of the bank.

Among the most glaring was SVB’s exposure to fragile start-ups. With the stock market virtually closed to new offerings, and venture capital firms becoming reluctant to part with their cash, tech firms were facing the sharpest falls in valuation since the dotcom bubble burst in the early 2000s. SVB provided banking services to such companies, making its deposit base vulnerable to a drought in venture capital funding. It also lent freely to them, expecting to be repaid not from the cash flows of the business, but from the eventual bonanza when new investors supplied another round of capital.

Highly unusually for a bank, SVB received warrants in many of the companies it financed, in effect a bet that any losses on its loan books could be covered if just a few of the companies went on to become unicorns. It was a wealth management operation for the VC and PE industry.

SVB’s lending to unprofitable start-ups surprised not only the short sellers, but also some of the bank’s own staff. “If you’re a banker at a traditional bank, your credit analysis is very quantitatively rigorous and there has to be clear analysis of how you get paid back,” says one former SVB banker. “[SVB’s] venture debt was more qualitative. [It was about] the conversations you have with investors about their willingness to support the company”. The risks inherent in SVB’s loan book spilled into public view after its failure last month. First Citizens Bank, which bought the portfolio from the Federal Deposit Insurance Corporation, negotiated a $16.5bn discount from a valuation supplied by the FDIC, equivalent to about 20 per cent, suggesting that many bidders were hesitant.

In the end, however, it was a different part of SVB’s balance sheet that caused the bank’s fall: its portfolio of supposedly safe bonds. Unlike debt owed by Silicon Valley start-ups, securities issued by the US government are virtually certain to be repaid in full. That does not stop their value from fluctuating, however: bond prices fall as interest rates rise, and that made SVB vulnerable to the financial health of its customers in a more subtle way. As venture capital-backed companies struggled to raise new money, their checking accounts began to run low, hastening the moment when SVB might have to sell bonds to meet withdrawals and book the ensuing losses.

At this point, SVB’s survival depended in large part on its chief executive, Greg Becker, whose public appearances were a third source of information about the bank’s health in its final months. He sought to articulate a plan for navigating those losses that would command the confidence of depositors and prevent a steady trickle of outflows from turning into an uncontrollable torrent. “We were preparing for [this],” he said. “With all this excess liquidity we have, first let’s make sure we’re investing it in a very conservative way.” The government bonds that SVB planned to hold to maturity were still useful collateral, even if they were declining in value. “Because it’s high quality, we can borrow against it for liquidity purposes,” said Becker. “We have no intention of selling it as we can borrow against it.” By then, however, many depositors had heard enough. Withdrawal requests began to surge. To meet them, Becker would ultimately be forced to unload $21bn worth of bonds at a loss, and launch a $2.25bn sale of SVB’s own shares. When no buyers could be found, the withdrawal requests came even faster.

Among the depositors to flee was Giridhar Srinivasan, a former Lehman Brothers employee who had recently raised $2mn for his business information start-up. Srinivasan finally succeeded in sending most of his company’s funds to a different bank. When SVB failed on March 10, his remaining account balance was just $55,000. ‘How did this happen?’ Less than a week after Srinivasan’s sleepless weekend came a disorienting few days for the Fed chair, Jay Powell. SVB had become the second-biggest bank failure in American history. “I mean, the question we’re all asking ourselves over that first weekend was, ‘How did this happen?’,” Powell later recalled. Answering that question is now the task of the Fed’s top official on banking supervision, Michael Barr, who assumed his post in July last year and has already called the collapse a “textbook case of mismanagement”.

Barr’s task will begin with a frank reassessment of the legacy of his Trump-appointed predecessor Randal Quarles, whose signature reforms shielded banks from intensive oversight so long as their assets did not exceed $250bn. Those reforms followed bipartisan legislation passed in 2018 that rolled back portions of the post-crisis Dodd-Frank law for small and midsize lenders. That resulted in less frequent stress tests, less onerous capital requirements and an exemption from the so-called liquidity coverage ratio rule, which requires banks to hold enough high-quality liquid assets that they can sell to cover outflows during times of stress.

Elizabeth Warren, the progressive Democrat from Massachusetts who had long opposed the rule changes, went so far as to say that the recent bank failures “were entirely avoidable if Congress and the Fed had done their jobs and kept strong oversight of big banks in place”. Bank lobbyists have called the rule changes a “red herring”, noting that the root cause was corporate mismanagement and poor investment decisions with what turned out to be highly mobile depositors. For his part, Quarles has argued that the SVB episode “didn’t have anything to do with the modest regulatory or supervisory refinements that we made”. Even if SVB had been subject to the full liquidity coverage rule it would not have made “any difference to the outcome”. The old rule, Quarles said, imposed extra liquidity requirements on banks that made extensive use of wholesale funding, deposits from other financial institutions, or other forms of “hot” money. He contended that it would have imposed few constraints on SVB, which used more conventional sources of funding. Hot money “has not generally been thought to be core deposits from your customers”, he added.

But Greg Feldberg, a former Fed staffer who is director of research for the Yale Program on Financial Stability, takes issue with that assessment. His calculations suggest that SVB would have fallen below the liquid assets threshold if it had not been exempted — proof, he says, that the Trump-era rule changes were “complicit in the run and failure at SVB”. Beyond marking his predecessor’s homework, Barr will have to contend with claims that supervisors failed to handle risks that became evident long before SVB’s implosion.

According to Barr, he only became aware of SVB’s exposure to interest-rate risk in February of this year. But problems had appeared in late 2021; supervisors identified issues with the way in which the bank was managing itself which they said could exacerbate the effect of an adverse shock. They flagged some of the deficiencies as “requiring immediate attention”. Despite the warnings, the bank did not fix the problems. It is unclear what actions regulators took next, beyond stripping the bank’s management of its “fair” performance rating, and replacing it with one that came with an automatic ban on SVB buying other banks.

Lawmakers at opposite ends of the political spectrum — Warren and Rick Scott, a Republican senator for Florida — have called for the internal watchdog who oversees the central bank to be replaced with a beefed-up inspector-general nominated by the president. “That at least reinforces some sense to the general public that there’s going to be real lessons learnt,” says Andrew Levin, a two-decade Fed veteran now at Dartmouth College, who views such a step as “imperative”. He has also called on the Fed to initiate voluntary stress tests for midsized lenders, similar to the capital reviews that helped to calm the panic stemming from the global financial crisis.

Beyond that, opinion is divided between those who think the 2018 regulatory changes need to be undone, and those who instead blame the debacle on the Fed’s failures. The Biden administration has sided squarely with the first camp, calling for the reversal of the Trump-era rules that relaxed oversight of smaller banks. That would mean more frequent stress tests, more stringent capital and liquidity requirements and a revival of the requirement that each institution submit a “living will” explaining the steps that should be taken to safely manage its failure.

Even without new legislation, Barr has hinted that the Fed is preparing to beef up its own rules governing midsized banks. But that process is likely to take years. “The question is how can we get supervision to once again pressure and probe management about their base case,” says Daleep Singh, who previously led the markets group at the New York Fed before serving as deputy director of Biden’s National Economic Council. “How can we ensure that supervisors are asking awkward questions, and at least unsettling the minds of management to see their blind spots?” Whereas the Biden administration sees weakness in the reforms passed by its predecessor, Republicans instead blame the Fed for failing to provide adequate oversight within the present rules. Some officials within the Fed have argued against wide-ranging changes of the regulatory regime. Among them is Michelle Bowman — a Trump-appointed governor — who recently said that, while “some changes may be warranted”, the bank failures were not “an indictment of the broader regulatory landscape”.

Proposals for new regulations have drawn even sharper attacks from some Republican lawmakers. “I think that’s what people hate about Washington,” Katie Britt, a Republican senator from Alabama, told Barr at congressional hearings investigating SVB’s collapse last month. “We have a crisis and you come in here without knowing whether or not you did your job. You say you want more. “That’s not the way this works. You need to be held accountable, each and every one of you.”